Guide section

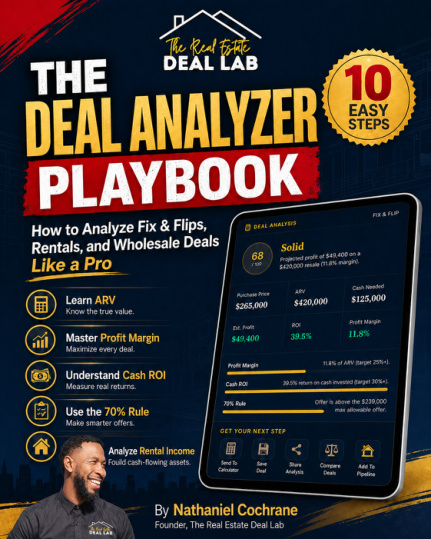

What a Real Estate Deal Analyzer Actually Does

A deal analyzer turns scattered property details into a structured decision, so you can compare price, risk, and upside without guessing.

A real estate deal analyzer is not just a calculator. It is a decision filter. The goal is to understand whether the opportunity deserves more time, a better offer, a different exit strategy, or a clean pass.

The Real Estate Deal Lab approach starts with the same question Nathaniel asks when looking at a live opportunity: what has to be true for this deal to work? That means purchase price, repairs, after repair value, rent, financing, timeline, and people all have to be tested together.

- Use one set of assumptions for a flip outcome.

- Use another set of assumptions for a rental outcome.

- Compare the numbers against the actual cash and time required.

- Decide whether the deal needs a lower offer, a partner, a different strategy, or no action.

Guide section

The Inputs That Matter Before You Run the Numbers

The most useful analysis starts with complete inputs, not optimistic guesses.

Most bad analysis starts before the spreadsheet opens. The purchase price may be clear, but repair scope, rent, insurance, taxes, financing cost, and closing timeline are often guessed too quickly.

Before you trust any score, collect the inputs that can move the result. Even a strong-looking deal can weaken if taxes reset, repair costs expand, rents are overstated, or the financing timeline creates extra holding cost.

| Input | Why it matters | What to verify |

|---|---|---|

| Purchase price | Sets the starting point for every exit strategy | Seller expectation, liens, closing costs |

| Repair budget | Can erase spread quickly | Scope, labor, materials, contingency |

| ARV or rent | Drives flip profit or rental income | Comparable sales, active rents, concessions |

| Financing | Controls cash needed and monthly cost | Rate, points, term, down payment, reserves |

| Timeline | Creates holding cost and execution risk | Permits, contractor schedule, sale or lease speed |

Guide section

How to Read a Fix and Flip Deal

A fix and flip works only when the spread remains healthy after repairs, financing, closing costs, holding costs, and selling costs.

A flip analysis should not stop at purchase price plus repairs. The real question is whether the finished sale price leaves enough room for the money, time, and risk required to complete the project.

Start with after repair value, then subtract purchase price, repair budget, closing costs, holding costs, financing costs, selling costs, and a contingency. If the remaining profit is thin before the project starts, the deal may not survive normal surprises.

- 1

Confirm after repair value

Use recent comparable sales that match condition, size, location, and buyer profile.

- 2

Build the repair scope

Separate must-do repairs from optional upgrades, then add a contingency for missed items.

- 3

Add time costs

Include loan payments, utilities, insurance, taxes, and delays between purchase, rehab, listing, and closing.

- 4

Set a minimum margin

The margin should justify the risk. A busy investor should not take construction risk for a weak spread.

Guide section

How to Read a Rental Deal

A rental deal should be judged by durable cash flow, reserves, financing, and whether the property still makes sense after realistic expenses.

A rental can look strong when the only comparison is rent minus mortgage. That is not enough. A serious rental analysis includes vacancy, repairs, capital expenses, management, taxes, insurance, utilities, and reserves.

The best rental deals create options. They can hold through normal vacancy, cover debt service, support maintenance, and still leave a path to refinance, sell, or improve income later.

- Monthly cash flow after debt service.

- Cash-on-cash return based on actual cash required.

- Cap rate before financing, so the property can be compared cleanly.

- Debt service coverage, especially if the lender requires it.

- Reserve needs for repairs, turnover, and slow leasing periods.

Guide section

Risk Flags That Should Slow You Down

The deal analyzer should surface risk, not hide it behind a strong headline number.

A deal can have a strong projected return and still be the wrong move. The risk flags matter because they show where the deal may break under pressure.

Nathaniel's operator lens is simple: the closer a deal is to your available cash, time, or experience limit, the more conservative the assumptions should be.

- Repair scope is not written down or priced by someone qualified.

- Comparable sales are old, too far away, or not similar.

- Rent assumptions depend on perfect tenants or premium pricing.

- Financing terms are not confirmed.

- The seller timeline requires you to move before diligence is complete.

- The deal only works if nothing goes wrong.

Guide section

How to Choose the Next Step

The purpose of deal analysis is action, a better offer, deeper diligence, a partner conversation, or a clean pass.

Once the numbers are in front of you, do not treat the score as the decision. Treat it as the start of the next conversation. A strong deal may still need better terms. A weak deal may become usable at a lower price. A confusing deal may need review before you risk earnest money.

Use the Deal Analyzer when you have enough inputs to test the deal. Use a fit call or advisory path when the question is no longer basic math and has become strategy, structure, funding, negotiation, or execution.

FAQ

Questions this guide answers

Sources and trust

Educational sources and disclosures

This guide is educational content from The Real Estate Deal Lab. It is not financial, legal, tax, lending, or investment advice. Use qualified professionals before making decisions that affect contracts, financing, taxes, insurance, or legal structure.